NAVIGATING THROUGH THE ASIAN RELUCTANCE IN IMPLEMENTING THE MODEL LAW: BRIDGING THE PACIFIC DIVIDE

Saurav Panda & Ahkam Khan*

- Introduction

In an increasingly interconnected world, global interdependence in trade has become a defining characteristic of modern economies, and the structures for undertaking international business have undergone a significant evolution. Global trade interdependence has led to cross-border investment flows creating multi-national corporates having assets, liabilities, debtors and creditors across jurisdictional borders. When the debtor is subject to the application of multiple domestic laws, it gives rise to various private international law issues.1 The complexity of global interdependence underscores the need for consistent legal frameworks for insolvency and restructuring. These frameworks ensure that creditors have a clear understanding of their rights and the recourse

available in the event of a company’s financial distress, leading to certainty and predictability, which in turn fosters confidence and promotes economic cooperation.

In an insolvency scenario, the most ideal economically efficient outcome lies in a collective and coordinated proceeding conducted in a single jurisdiction with worldwide recognition and enforceability. The coordination of proceedings and cooperation between judicial and administrative agencies in different jurisdictions aids “the goal of maximising the value of the debtor’s worldwide assets, protecting the rights of the debtors and creditors and in furthering of the just administration of the proceedings”.2 With this thought and rationale, the United Nations Commission on International Trade Law (UNCITRAL) issued the Model Law on Cross-Border Insolvency (MLCBI) on 30 May 1997.

The MLCBI seeks to equip national insolvency laws with a more modern, harmonised and fair framework to deal with insolvencies where the assets of the debtor lie in more than one state or where the creditors of the debtor belong to more than one state.3 The MLCBI was conceptualised as a framework which could supplement the national laws and foster the application of uniform and consistent principles in cases of cross-border insolvency. Rather than attempting an overhaul and unification of all substantive insolvency laws across the globe, the MLCBI

respects the procedural differences in national laws and seeks to adopt a middle path, in which the national

insolvency framework continues to prevail but in a fairer and more harmonised environment marked by the

principles of:

(i) cooperation and coordination – both judicial and administrative;

(ii) access – to assets and foreign courts;

(iii) recognition – of foreign proceedings, foreign representative and foreign creditors; and

(iv) relief – in the nature of interim, mandatory and discretionary relief available at different instances.4

The MLCBI has emerged as the most popular choice globally for adoption of a cross-border insolvency framework in the domestic legislations in view of the flexibility it offers, and several states have adopted it with bespoke modifications suiting their jurisdictional needs. As of January 2024, 60 states have enacted legislation either based on or influenced by the MLCBI.5

However, on closer analysis, it is observed that only 10 countries have adopted the MLCBI in Asia. This statistic

paints a grim picture for the largest and most populous continent in the world, especially if we consider the

position that Asia holds in the global economy. Being home to nearly 60% of the world’s population,6 Asia provides a substantial domestic market that fuels consumer demand, workforce availability and economic growth.

In addition to demographic advantages, several countries in Asia are recognised for being major centres of manufacturing and industrial activity. Several of the region’s economies are characterised by a strong industrial base, extensive production capabilities and integration in global supply chains. The continent’s economic landscape is marked by significant influence on international trade and investment flows, making it an indispensable component of the world economy.

We have carried out a survey among certain leading practitioners in several Asian jurisdictions to analyse the key drivers for the adoption (or, as applicable, reluctance in the adoption) of the MLCBI.

We have also sought to contrast the manner of implementation of cross border insolvency in two jurisdictions that have incorporated the MLCBI, Japan and Singapore (highlighting the unique manner of adoption and the different factors responsible for it).

Focusing on the need to facilitate harmonisation in cross-border insolvency laws, the paper aims to contribute to understanding the complexity of cross-border insolvency reforms in Asia.

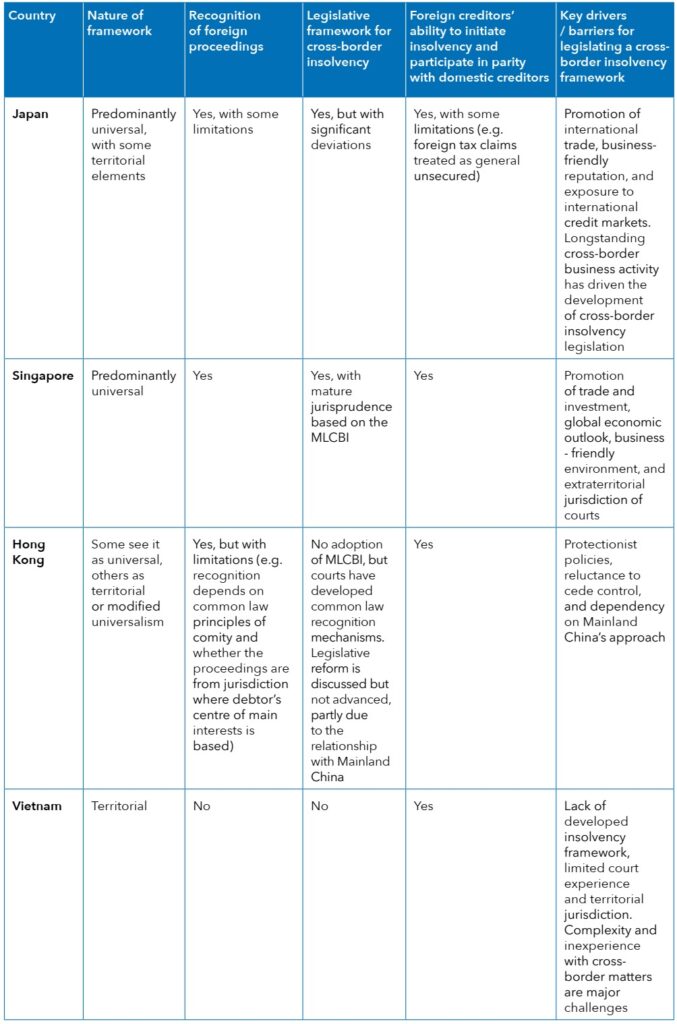

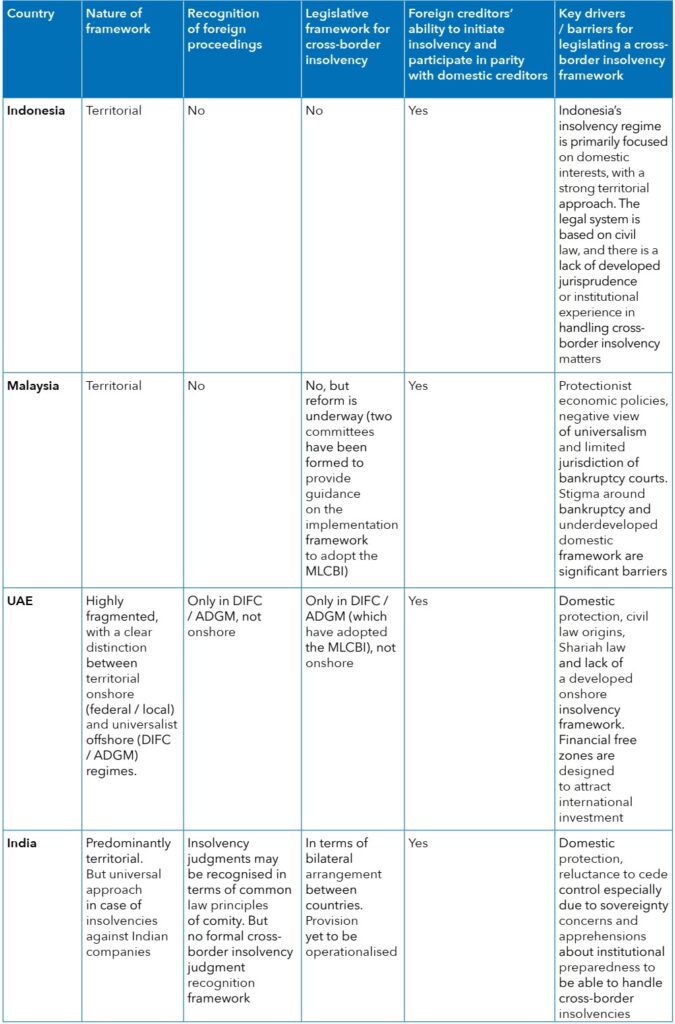

2. Survey-based analysis in Asian jurisdictions7

In order to understand the factors responsible for the slow progress in adoption of the MLCBI in Asia, we have conducted an analytical study based on survey responses from several insolvency and legal practitioners regarding the status of cross-border insolvency laws in their respective Asian jurisdictions. The detailed survey covers certain Asian jurisdiction(s) which have either:

(i) adopted the MLCBI – Japan and Singapore;

(ii) adopted the MLCBI only in certain special zones within the jurisdiction – the UAE, which has adopted the MLCBI in the Abu Dhabi Global Market (ADGM) and the Dubai International Financial Centre (DIFC);

(iii) neither adopted nor proposed the adoption of the MLCBI – Hong Kong, Vietnam and Indonesia; or

(iv) not adopted the MLCBI but have proposed legislation based on it – India and Malaysia.

As part of the survey, the practitioners were asked several questions in order to better understand the applicability of their domestic insolvency legislation to cross border insolvency, the status of adoption of a cross-border insolvency framework, and the key drivers or barriers (as applicable) to the enactment of the MLCBI. Some of the key questions posed in the survey included:

(i) Whether the application of insolvency laws in the jurisdiction is universal or territorial.

(ii) Whether the domestic insolvency framework allows administration of foreign assets in a domestic proceeding.

(iii) Whether the domestic insolvency framework recognises the administration of domestic assets in a foreign proceeding.

(iv) Whether the domestic insolvency framework recognises claims from foreign creditors and allows the initiation of insolvency on an application by a foreign creditor. And, if yes, whether claims of foreign creditors are treated at par with claims of domestic creditors.

(v) Whether the jurisdiction has a legislative framework governing cross-border insolvency.

(vi) If the answer to (v) is yes, which factors contributed to the jurisdiction legislating a framework for cross-border insolvency.

(vii) If the answer to (v) is no, which factors are the probable reason for the reluctance of the jurisdiction in legislating a framework for cross-border insolvency.

(viii) If answer to (v) is no, whether any legislative framework governing cross border insolvency been proposed/contemplated in the jurisdiction.

Based on the analysis of the results of the survey, a comparative summary of key features in the insolvency framework of the surveyed Asian jurisdictions is set out in the table below:

On a deeper analysis of the survey responses, some important themes emerge, which are set out below.

2.1 Strong divide between universalism and territorialism

Free market zones in the UAE and Singapore have robust universalist frameworks, with legislative support for the recognition of foreign insolvency proceedings. Hong Kong, while not having adopted the MLCBI, applies modified universalism through the common law. Indonesia, Malaysia, Vietnam and onshore UAE maintain a territorial approach, with limited or no recognition of foreign insolvency proceedings and no comprehensive legislative frameworks as these jurisdictions prioritise domestic interests.

The overall trend appears to be towards greater adoption of cross-border insolvency frameworks in jurisdictions with open economies, mature legal systems and a strong orientation towards international trade and investment, while others remain domestically focused and cautious in the adoption of universalist frameworks.

2.2 Access of foreign creditors to domestic proceedings not contingent on MLCBI adoption

Even though many Asian jurisdictions have not formally adopted the MLCBI, there is a notable trend towards recognising the rights of foreign creditors to participate in domestic insolvency proceedings (i.e. just as any other creditor, and having the same rights as domestic creditors). For example, even some territorial regimes like Vietnam and Malaysia allow foreign creditors to file claims and be treated at par with domestic creditors in insolvency processes.

This practice demonstrates a willingness to accommodate international stakeholders and suggests that concerns over ceding domestic control to foreign interests may be less pronounced than often assumed. The openness to foreign creditor participation reflects a pragmatic approach to cross-border insolvency, driven by the realities of international trade and investment. Such recognition not only aligns with global commercial expectations, but also lays a practical foundation for the eventual adoption of and smoother transition towards the MLCBI in the future, as it indicates that the legal and judicial systems in these jurisdictions are already accustomed to balancing domestic and foreign interests within insolvency proceedings.

2.3 Insolvency as “in rem” proceedings having “erga omnes” effect

Even in Asian jurisdictions that maintain territorial insolvency regimes and have not adopted the MLCBI, there is a clear domestic recognition that insolvency proceedings operate “in rem” (affecting the debtor’s assets as a whole) and “erga omnes” (binding against all parties, both domestic and foreign). This approach inherently accepts that the resolution of insolvency is not merely a matter of local interest but rather has implications for all assets and all stakeholders of the debtor.

The willingness to apply insolvency outcomes universally and to bind all parties to the result demonstrates a pragmatic understanding of the interconnectedness of modern commerce. It also suggests that these jurisdictions are not fundamentally opposed to the idea of ceding some degree of control in favour of a more harmonised, international approach. The foundational acceptance of the “in rem” and “erga omnes” principles within domestic insolvency law (agnostic to a party’s nationality) provides a conceptual basis that could ease the transition to the MLCBI, as courts and practitioners may already be familiar with the idea that insolvency outcomes must be recognised and respected by all.

2.4 Effect of enactment of framework governing cross-border insolvency on international trade or inbound investments

In relation to the question regarding whether the presence (or lack) of a framework governing cross-border insolvency has any effect on international trade or inbound investments in their states, the majority of the respondents answered with essentially a “maybe”. While these jurisdictions may lack studies suggesting a clear dependence of international trade / inbound investments on insolvency frameworks, the respondents’ answers suggest a nuanced relationship between insolvency law and economic activity.

The ambivalence seems to indicate that while insolvency frameworks are recognised as important, they are not viewed as the sole or decisive factor influencing international trade or foreign direct investment (FDI) inflows. Other considerations such as overall economic policies, market openness, legal certainty and the perception of the jurisdiction as business friendly may play equally or more significant roles in attracting international commerce and investment.

Although a robust and predictable insolvency regime can enhance investor confidence by providing clarity and protection in the event of debtor distress, its absence does not necessarily deter trade or investment outright. Instead, investors and trading partners may weigh insolvency frameworks alongside a broader set of legal, economic and political factors.

In some jurisdictions, the lack of a developed cross-border insolvency regime is mitigated by other strengths, such as mature domestic insolvency jurisprudence, established commercial practices, or the presence of financial centres with more advanced legal infrastructure (as seen in Hong Kong’s modified universalism approach). Therefore, while the existence of a comprehensive cross-border insolvency framework can be a positive signal to international investors and trading partners, its ultimate impact on international trade and FDI inflows is likely to be influenced by the interplay of multiple other factors that collectively shape the jurisdiction’s attractiveness as a destination for cross-border economic activity

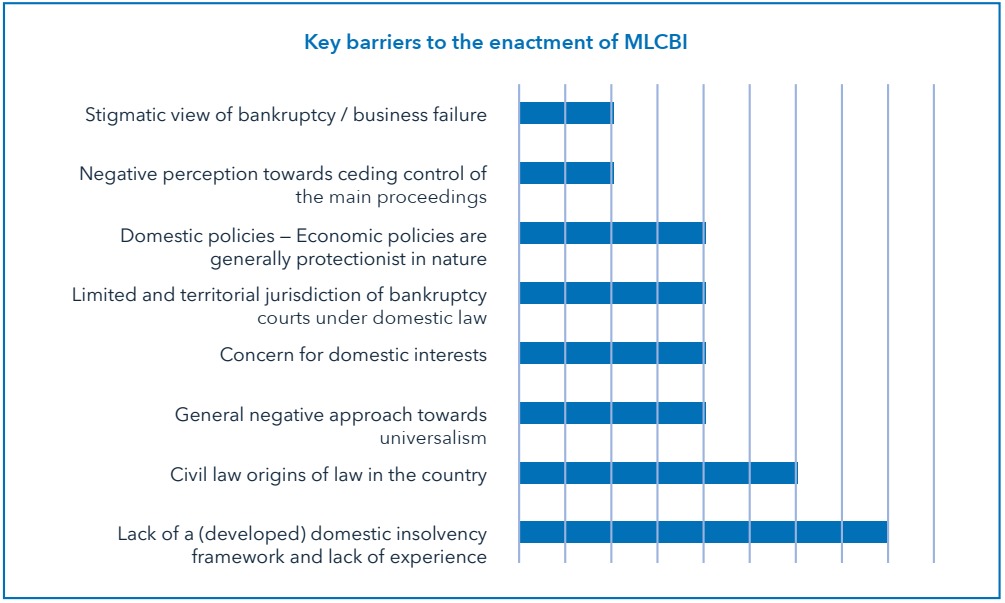

3. Reasons for reluctance in adoption of the MLCBI in Asia: why they may be misplaced

Based on the survey responses, the following key reasons were highlighted for the reluctance to adopt the MLCBI or any similar framework for cross-border insolvency.

3.1 Concerns over sovereignty and judicial control

From the results of the survey-based study for jurisdictions that are yet to adopt the MLCBI in Asia, it appears that many Asian countries continue to be wary of ceding control over domestic insolvency proceedings to foreign courts or representatives. There appears to be an apprehension that the MLCBI could undermine national sovereignty by allowing foreign representatives to participate in local proceedings or by requiring local courts to recognise foreign proceedings.8

It is also worthwhile to point out that many of the Asian economies have had a history of colonial rule and subjugation of their economies by imperialist powers and, therefore, have a strong inclination to ensure that any cross-border insolvency framework does not impede their sovereignty. For these reasons, many Asian economies seem to have a deep-rooted belief in retaining full discretion over domestic insolvency proceedings.

However, this concern appears to be misplaced for the following reasons. Firstly, the MLCBI is only a procedural framework and does not demand substantive harmonisation of domestic laws. Secondly, the MLCBI itself provides mechanisms for sufficient safeguards against the compromise of sovereignty of the adopting states – including:

(i) article 6 of the MLCBI, which allows domestic courts to refuse recognition to foreign proceedings, if it would be manifestly contrary to public policy; and (ii) sufficient discretion may be left to domestic judges for the grant of appropriate relief on a case-to-case basis (such as in the case of the MLCBI as adopted by Japan).

3.2 Protectionist / nationalistic sentiment and fear of prejudice to domestic creditors

Ordinarily, there is a concern that adopting the MLCBI could damage what the state’s concept of national interest is, besides causing a disadvantage to local creditors in favour of foreign creditors, especially in cases where foreign main proceedings are recognised and local assets are administered under foreign law.9 This effect has specifically become more pronounced in the current global political environment, where protectionism is likely to continue rising. This trend is largely driven by factors such as increasing geopolitical tensions, a desire for national self-sufficiency and a push to secure critical resources.10 Many countries are implementing new trade barriers, including tariffs and non-tariff measures, to protect domestic industries and their trading partners are engaging in retaliatory measures.

However, while there may be reluctance in certain Asian economies to adopt the MLCBI on this account, there are some critical points indicating that the concerns may be unfounded. Firstly, the MLCBI includes sufficient safeguards to protect local creditors. For instance, article 21 allows courts to tailor relief to ensure fairness, and articles 20(2), 21(2), 22 and 23(2) have the capability of adequately preserving the rights of domestic creditors under local law.

Secondly, statistics have shown that, in jurisdictions that have implemented the MLCBI, domestic creditors have not been systematically disadvantaged; rather, the law has facilitated more equitable and efficient asset distribution. Recent United States studies have found that Chapter 15 (the United States cross-border insolvency

framework) has provided greater protection to both foreign and United States creditors and has maximised overall liquidation or reorganisation values.11

Further, the results of our survey-based study suggest that the domestic insolvency frameworks in Asian jurisdictions already allow the participation of foreign creditors in domestic proceedings. These creditors are generally treated at par with domestic creditors (both in terms of rights to initiate the proceedings and the right to file a claim in the proceedings), thereby reflecting a moderated approach to the treatment of foreign creditors, irrespective of whether a state has adopted the MLCBI. These states are therefore less likely to be wary of the MLCBI prejudicing domestic creditors at the altar of recognition and access to foreign creditors. Therefore, the countries may need to re-think their conception of “national interest”. Enacting of the MLCBI may, in fact, turn out to be more beneficial than prejudicial for local creditors.

3.3 Civil law traditions and judicial conservatism

Several Asian jurisdictions operate under civil law traditions, where judges are less inclined to interpret laws and exercise discretion, making them hesitant to adopt a framework that relies heavily on broad principles of judicial discretion and cooperation.12 These states are hesitant that the MLCBI’s principles may not align seamlessly with local insolvency laws.

It must be understood that the MLCBI is intentionally flexible and can be adapted to fit different legal traditions. Besides common law Asian countries like Singapore, countries having civil law or hybrid legal origins such as Japan and South Korea have also implemented the MLCBI, demonstrating its practical adaptability.

3.4 Underdeveloped domestic frameworks and need for capacity building

Some countries lack a robust and modern domestic insolvency regime, which is often made out to be a prerequisite to effectively implement the MLCBI since a lack of familiarity with insolvency frameworks may lead to hesitation in adopting an international framework. It assumes further significance as the MLCBI requires cooperation and coordination among the insolvency courts and representatives of all the relevant jurisdictions involved. While such arguments may have some merit, it can equally be posited that adoption of the MLCBI could also serve as a catalyst for domestic reform since international best practices would raise the bar for efficiency, transparency and investor confidence. In fact, in the context of the United States, studies suggest that multinational debtors from countries with strong domestic insolvency laws (based on global standards) gain greater benefits from cross-border recognition in terms of the MLCBI.13

In this regard, it may be important to highlight the performance of Asian economies which have not adopted the MLCBI (which were subject matter of the survey) in the “insolvency resolution efficiency” component of the World Bank’s Doing Business Report:

(i) Hong Kong – ranked 45;

(ii) Indonesia – ranked 38;

(iii) Vietnam – ranked 122; and

(iv) Malaysia – ranked 40.

This compared to the performance of the Asian economies which have adopted the MLCBI:

(i) Japan – ranked 3;

(ii) South Korea– ranked 11; and

(iii) Singapore – ranked 27.14

The above rankings certainly indicate that the countries which have implemented the MLCBI have clearly performed better on the “resolving insolvency” parameter. Further, the countries with modern insolvency frameworks, including cross-border protocols, and more developed legal rights for creditors, have seen higher FDI inflows. Indeed, in several states, net FDI inflows have substantially increased following progressive and creditor-friendly amendments to the domestic insolvency laws.15

To counter the argument regarding familiarity with insolvency principles, the adoption of the MLCBI can be accompanied by capacity-building initiatives, as seen in Singapore, where judicial training and public-private dialogues facilitated smooth implementation.16 Further, global institutions like the World Bank, UNCITRAL and INSOL International, along with regional institutions such as the Asian Development Bank, offer technical assistance to countries considering adoption, helping to bridge knowledge gaps.17

3.5 Limited exposure to cross-border insolvencies and consequent lack of political will

Some policy makers argue that the volume of cross-border insolvency cases involving Asian companies is relatively low, making comprehensive reform seem unnecessary or premature. As a result, governments may not see the immediate economic or political benefit in reforming cross-border insolvency laws.

While the number of cross-border insolvency cases may be lower in some Asian economies, globalisation and increasing foreign investment are rapidly changing this landscape. Further, the engagement of Asian economies with the rest of the world has undergone a significant transformation in recent years. While traditionally, the focus was primarily on foreign entities investing in or acquiring assets within Asia, this dynamic is evolving as Asian conglomerates themselves are increasingly expanding their footprint beyond their home countries and establishing a presence in global jurisdictions. The rapidly increasing cross-border investment in Asia, coupled with the growth in the number of multi-national Asian conglomerates, is increasing the likelihood of cross-border insolvency cases across Asian jurisdictions.

Early adoption of the MLCBI can help economies prepare for future challenges and attract foreign investment by providing legal certainty,18 as studies already suggest that enactment of the MLCBI may increase inbound cross border acquisition activities and FDI inflows.19 Simultaneously, the adoption of the MLCBI by Asian jurisdictions may also allow coordinated proceedings in insolvency matters involving global Asian conglomerates, which may lead to easier access to global assets and higher recoveries for creditors.

4. Differing manner of adoption of the MLCBI in Asian jurisdictions

Having understood the key reasons for reluctance regarding adoption of the MLCBI in Asia and our views on how some of them may be misplaced, it is equally worthwhile to analyse the manner in which the MLCBI has been adopted so far in Asia.

The adoption of the MLCBI in Asia began in 2000, with Japan being one of the first countries to have adopted the MLCBI in the world. Thereafter, a few other Asian countries have adopted MLCBI such as South Korea, the Philippines and Singapore. It is however noted that there is a lot of divergence in the manner in which the MLCBI has been adopted by different economies in Asia.

To obtain a deeper insight into this divergence, we have sought to illustratively deal with two Asian jurisdictions that are both differently placed and have different motivations, and have taken significantly very distinct paths in their adoption of the MLCBI: Japan and Singapore.

Japan’s cautious yet incremental approach towards universality and Singapore’s pragmatic adaptation of universalist principles offers valuable insights into the different approaches in the implementation of MLCBI, depending on each country’s unique position and outlook.

4.1 Japan

Japan was one of the first countries to adopt legislation implementing the MLCBI. In 2000, Japan enacted the “Act on Recognition of and Assistance for Foreign Insolvency Proceedings” (RAFIP), which bestowed upon the Tokyo District Court the power to recognise and provide assistance in respect of foreign insolvency proceedings in Japan.

Prior to the enactment of the RAFIP, Japan employed a pure territorialism approach in respect of its insolvency laws. The insolvency law neither recognised the effect of Japanese proceedings to foreign countries nor recognised the effect of foreign proceedings in Japan.20

While the RAFIP is modelled on the MLCBI, Japan has incorporated several deviations from the original construct of the MLCBI, some of which are detailed below.

(i) Definition of a “foreign proceeding”: The definition of “foreign proceeding” adopted in the RAFIP differsfrom the MLCBI, as a foreign proceeding is defined in RAFIP as a proceeding filed in a foreign country which is equivalent to a Japanese insolvency proceeding, thereby restricting the scope of proceedings which may be recognised in Japan. Further, the determination of whether the recognition proceedings correspond to one of the domestic Japanese insolvency proceedings also depends on the judge’s discretion, considering that the domestic Japanese law lacks provisions defining these insolvency proceedings.21

(ii) Wide public policy exception: Japan has diluted the public policy exception, and recognition of a foreign proceeding can be refused if it is “contrary to the public policy” of Japan, as opposed to the more stringent “manifestly contrary to public policy” standard under MLCBI, which can only be applied to exceptional

scenarios involving matters of fundamental importance.22

(iii) Additional conditions for denial of recognition: The RAFIP sets out additional conditions for the denial of recognition,23 including if the petition is made for an “unfair purpose”, the foreign proceeding not having any effect on the debtor’s assets in Japan, or if the recognition or assistance is manifestly filed in bad faith or would be against public order or good public morals in Japan. In contrast, the MLCBI requires the recognition of foreign proceedings if they meet the formal requirements and a public policy violation is not in play,24 which is intended to ensure expedited relief by limiting the examination to the jurisdictional pre-conditions so that the receiving court does not embark on roving enquiries.

(iv) Weaker effects of recognition: The RAFIP does not provide for an “automatic stay” upon recognition of a foreign proceeding. However, it stipulates that the court may grant discretionary relief to the debtor or its assets in Japan, after the recognition of the foreign proceeding, irrespective of whether the foreign proceeding is a main proceeding or a non-main proceeding.

(v) Concurrent proceedings: Like the MLCBI, the RAFIP allows the continuation / initiation of a local proceeding, even when a foreign proceeding has already been initiated. However, for coordination purposes, the RAFIP takes a different approach and applies the “only one proceeding for one debtor” rule, which prioritises the local proceeding over the foreign proceeding, unless it is a rare case where the foreign proceeding is the main proceeding in the best interests of creditors, and its recognition would not unjustly violate or prejudice the interests of Japanese creditors.

4.2 Singapore

On 30 March 2017, Singapore passed the Companies (Amendment) Act 2017, which adopted the MLCBI in Singapore. The Senior Minister of State for Law had then announced that it would pave the way for Singapore to become the primary jurisdiction for commercial transactions in the world, and allow predictable out comes and certainty in cases of cross-border insolvencies of Singaporean entities by reducing the desirability of forum shopping.25 Contrary to Japan, Singapore’s adoption of the MLCBI appears to be much less deviant in both letter and spirit from the original construct of the MLCBI, and the approach appears to be far more progressive. Some of the key deviations from the original text of the MLCBI as adopted by Singapore are outlined below.

(i) Narrow public policy exception: Singapore has made a similar deviation as Japan and lowered the threshold for denial of recognition, with reference to a “contrary to public policy” standard rather than a “manifestly contrary to public policy” standard. Interpreting this standard in Zetta Jet 1,26 the High Court recognised that the omission of the term “manifestly” was deliberate and conscious and, therefore, the standard for the application of the public policy exception was lower in Singapore. Subsequently in Re PT Garuda Indonesia (Persero) Tbk,27 however, the court held that mere omission of the term “manifestly” was insufficient to conclude that a lower threshold for finding a breach of public policy was intended. In this context, the Court noted that the word “manifestly” was used only to emphasise that the exception should be used restrictively28 and held that “its inclusion is to make explicit what was always implicitly understood to be the test”. Therefore, the Court disagreed with Zetta Jet 1 and held that omission of the term “manifestly” in Singaporean law did not alter the standard of “public policy” contemplated under the MLCBI.

(ii) Relevant date for determination of centre of main interests (COMI): While the MLCBI is silent on the relevant date for determination of COMI, by way of judicial orders Singaporean courts have applied the United States approach of determining COMI on the date of the recognition application (as opposed to the European Union or the United Kingdom, where COMI is considered on the date of the application to open the foreign proceedings).

(iii) No unfavourable outlook towards COMI shift: In Zetta Jet 2,29 the High Court of Singapore held that a COMI shift, subsequent to the date of the foreign insolvency application, may still be permissible to a jurisdiction where substantial connections exist even if the shift occurred after the date of the foreign insolvency application. Courts in Singapore have preferred to take a more liberal outlook towards any purported changes in COMI to recognise the applicant’s autonomy and to give effect to any preference exercised by the debtor, subject to any public policy concerns.

(iv) Wider definition of foreign proceeding: While the MLCBI links the definition of “foreign proceeding” only to a proceeding pursuant to a “law relating to insolvency”, the Singapore law30 provides a wider ambit of “law relating to insolvency or adjustment of debt”, thereby extending the definition of foreign proceeding to apply to even solvent proceedings. The Singapore Court of Appeal has held that there is no requirement for a debtor to be insolvent or in severe financial distress before a proceeding concerning that company may be recognised as a foreign proceeding in Singapore.31

5. Factors affecting the adoption / implementation of the MLCBI in Asian jurisdictions

It is interesting to observe that jurisdictions within Asia have opted for different approaches in adopting the MLCBI. In this section, we analyse the different factors which may have been responsible for the divergence of approaches in the manner of adoption of the MLCBI by different Asian jurisdictions.

5.1 History of the legal system

The origins of the legal system in a state have a great historical bearing on the judicial powers of the courts in that jurisdiction.

While common law jurisdictions are marked by general and discretionary judicial application of the principles of fairness and equity, civil law jurisdictions both structurally and historically discourage the exercise of judicial discretion. In a civil law jurisdiction, Professor AN Yiannopoulosin describes the process of “judicial determination” as one involving “always determination of issues in accordance with the requirements of formal logic”, where “rules of law furnish the major premise, fact situations form the minor premise, and the conclusion follows with logical necessity”, and one where “there is no room for discretion because formal logic is compelling”.32

In this context, it is pertinent to mention that the MLCBI only lays down a broad set of principles for the grant of relief by the court of the enacting state. Naturally, such a broad set of principles presupposes the exercise of judicial discretion by the court at the time of grant of relief. Therefore, one likely reason for the divergence in approach between Singapore and Japan is likely to be the different legal origins in both jurisdictions. While common law jurisdictions like Singapore and India may be more amenable to adopting and implementing the MLCBI without material deviations, jurisdictions such as Japan (which follow the civil law and inherently discourage the exercise of judicial discretion) may have reservations due to perceived contradictions with the core principles of their legal system and jurisprudence.33 Accordingly, where Japan lacks an explicit domestic law solution, they have preferred to avoid adoption of the uniformity and harmonisation of the MLCBI.

Jurisdictions which have historical ties to the British Empire or have historically adopted the elements of the common law system are therefore more likely to adopt the modified universalist approach recommended under the MLCBI. When adapting the MLCBI to domestic law, such countries are less likely to suggest any material deviations. This observation is relevant in the context of Asian economies such as Singapore (a common law country) and the Philippines (a mixed law country having common law influence), which have already adopted the MLCBI, and India and Malaysia (both common law countries) which are currently mulling over proposed legislation based on the MLCBI.

5.2 Economic conditions prevailing in the jurisdiction

The approach towards adopting international legal conventions and globally accepted principles, especially in the context of economic laws, is also a function of the openness of the national economy to the outside world. A conservative and closed domestic economy is much more unlikely to be incentivised by principles that benefit or promote transnational trade than an economy aiming to capitalise upon foreign direct investment.34

As an example, just before the enactment of the RAFIP, Japan had to hurry in enacting the Civil Rehabilitation Law because of the burst of the bubble economy and the boom in the insolvency of small and middle-sized companies.35 The rising number of insolvent companies provided an impetus for the recognition of cross-border insolvency, since many of these companies were operational in multiple jurisdictions. The economic condition in Japan at the time was therefore one of the reasons behind the enactment of the RAFIP. On the other hand, Singapore’s economy thrives on cross-border business interests since it is a global commercial hub. Its strong desire to project itself as a jurisdiction with harmonised rules for cross-border insolvency reflects in the fulsome effect its gives to the recognition of foreign insolvency proceedings.

5.3 Existing approach towards protection of the national interest

Most of the divergences from an international treaty or convention are sought to be justified by enacting states on the grounds of “national interest”. In the context of cross-border insolvency, Lord Peter Millet observed that “no branch of the law is moulded more by considerations of national economic policy and commercial philosophy”.36 The need to protect the interests of the domestic economy, local revenue and sovereign interests may far outweigh the incentive to appease an international community of investors.

States which traditionally are exclusively territorialist in their approach, such as Japan and Indonesia (including under other prevailing laws), are more likely to either not adopt international treaties or to seek carve-outs from them to protect their perceived sovereignty. While such jurisdictions may seek to recognise foreign insolvency proceedings, there is a resistance to fully commit to give effect to this recognition. Given that the insolvency laws in Japan had traditionally been territorial in their operation, Japan adopted a conservative approach while enacting the MLCBI

and diverged on several subjects, in its bid to simultaneously protect its perceived national interest.37

However, countries such as Singapore, which have already been moving to a moderately territorialist approach, are more likely to give wholesome effect to the modified universalism approach under the MLCBI. Even prior to the adoption of the MLCBI by Singapore, the courts had recognised administration orders made by English courts and held that administrators of an English company would have the same powers over the company’s property as they had under English law.38

Some jurisdictions such as the UAE, which have special zones for financial and commercial activities (i.e. the ADGM and the DIFC in the UAE), have taken a different approach and only adopted the MLCBI in these respective special zones. Such a framework is also supported by the fact that the ADGM39 and (partly) the DIFC operate on common law principles,40 with the basic objective of fostering financial and commercial activities and a special focus on the “ease of doing business”. On the other hand, the mainland UAE continues to follow a civil law system based on Sharia law. This framework allows the UAE to leverage business advantage and investments through these special zones, without ceding its domestic interests in ordinary national subjects.

Therefore, it is quite clear that even where the MLCBI has been adopted, it is marked by differing approaches given the unique position and the various economic and other national interest concerns of each adopting jurisdiction. The adoption of the MLCBI is not a one-size-fits-all exercise. The MLCBI recognises this and allows for

flexibility to suit the unique concerns of the respective jurisdiction.

6. Recent developments in cross-border insolvency laws in Asia

The proverbial tide appears to have already started turning in Asia. Some recent events are encouraging, indicating an impetus towards having in place a more robust cross-border insolvency framework. It is even more encouraging to note that some of these jurisdictions have already taken initial steps in framing up a cross-border insolvency framework by way of adopting the MLCBI with some deviations.

6.1 Malaysia

Malaysia, which had previously been completely territorial in its approach has, in line with the current Government’s strategy to implement sustainable economic growth and attract foreign investment, recently announced that it is proposing to adopt the MLCBI.41 The Malaysian Government has also formed two committees for providing guidance on the implementation framework: (i) the Cross-Border Insolvency Reform Main Committee, tasked with setting broad policy aligned with Malaysia’s economic priorities; and (ii) the Cross- Border Insolvency Reform Working Committee, tasked with providing the framework for integrating the MLCBI in Malaysia.42 It is expected that the draft law will be tabled in the Malaysian Parliament later in 2025.

6.2 Vietnam

On 4 February 2025, the People’s Supreme Court published a draft of the Amended Law on Bankruptcy for public consultation, aiming to supersede the current Law on Bankruptcy No. 51/2014/QH13 dated 19 June 2014.43 As part of the Amended Law, the Vietnamese courts are empowered to assist with foreign bankruptcy proceedings. This includes actions such as verifying, inventorying, valuing, liquidating and recovering assets of enterprises relevant to foreign bankruptcy cases. The draft also introduces detailed provisions for recognising and enforcing foreign courts’ bankruptcy judgments in Vietnam. It outlines the authority of Vietnamese courts and specifies circumstances under which foreign bankruptcy decisions may not be recognised domestically. The finalised Amended Law, after the conclusion of the public consultation process, is expected to be submitted by the end of May 2025 and the anticipated effective date for the Amended Law is 2026.44

6.3 India

India presently lacks any comprehensive cross-border insolvency framework. The body of law on cross-border insolvency is contained in two sections (sections 234 and 235) of the Insolvency and Bankruptcy Code 2016 (IBC).

These provisions only extend to: (i) give effect to any bilateral arrangements between India and any other country in relation to cross-border insolvency; and (ii) allow the adjudicating authority to issue a letter of request to a court in the country with which India has a bilateral agreement.

On 20 June 2018, the Ministry of Corporate Affairs (MCA) had proposed Draft Part Z (Part Z), modelled on the MLCBI, for insertion as an independent chapter in the IBC to govern the cross-border insolvency framework in India. Further, in 2020, the MCA had constituted the Cross-Border Insolvency Rules / Regulations Committee (CBIRC) with the objective of developing a comprehensive framework for implementing cross-border insolvency provisions, based on the MLCBI.45

The CBIRC submitted its report to the MCA on 15 June 2020 and the report was made available for public consultation in November 2021.46 Despite the Part Z and CBIRC report having been published for public consultation in 2018 and 2021 respectively, no cross-border insolvency provisions have yet been notified in India. Recent media reports suggest that the Central Government may be seeking to table an IBC Amendment Bill, which may include provisions for the introduction of cross-border insolvency.47

7. Conclusion

With Asian countries increasingly becoming global manufacturing and service outsourcing hubs, they are likely to witness exponential growth in cross-border business. As global trade and cross-border investments increase, these jurisdictions may eventually be forced to reconsider their positions, particularly as they seek to integrate more fully into the global economy and attract foreign investment. Without a harmonised legal framework, cross-border insolvency proceedings can be complex, costly and time-consuming, potentially leading to inefficient outcomes and discouraging foreign investment.

The MLCBI provides a consistent and internationally recognised framework for managing insolvencies that involve multiple jurisdictions, which enhances legal certainty and predictability. This consistent framework facilitates the optimal management of cross-border insolvency, benefiting debtors, creditors and other stakeholders by minimising losses and maximising asset recovery, including by enhancing the possibility of tracing and the recovery of assets across national borders through judicial and administrative cooperation. This is especially crucial for multinational companies and foreign investors / creditors operating in these jurisdictions, as it reassures them that their rights will be respected and that they can recover their claims efficiently, even in complex cross border insolvency cases.

While several Asian jurisdictions have traditionally been quite reluctant in the adoption of the MLCBI, due to concerns about safeguards for domestic interests, protection of sovereignty and the capacity of the domestic insolvency framework, it is pertinent to highlight that there are several safeguards within the MLCBI which could adequately safeguard the domestic interests of Asian economies. Delay in adoption of the MLCBI could significantly impact the prospects of insolvency resolution for Asian conglomerates having business interests all over the globe, in addition to potentially impacting FDI inflows. The examples of Japan and Singapore have clearly shown that the MLCBI does offer a great degree of flexibility to avoid a one size fits all solution, by enabling adoption with deviations as appropriate to each jurisdiction, without materially deviating from the spirit of modified universalism as envisaged by the MLCBI.

Recent developments have been encouraging, with a few Asian jurisdictions taking initial steps towards adoption of the MLCBI. By adopting the MLCBI and overcoming their traditional reluctance towards it, Asian jurisdictions can enhance their attractiveness as investment destinations, promote financial stability and provide improved domestic enterprise with access to global capital markets, thereby fostering economic growth and development.

Footnotes

- Ian F Fletcher, The Law of Insolvency, 4th ed, Sweet & Maxwell (2009). Examples of these issues may include recognition and enforcement of foreign court decisions, recognition of claims of foreign creditors, difference in priorities of creditor claims in different jurisdictions or issues surrounding the control and disposal of assets located in foreign jurisdictions.

- The World Bank, Principles and Guidelines for Effective Insolvency and Creditor Rights Systems (2016) https://documents1.wordbank.org/curated/en/518861467086038847/pdf/06399-WP-REVISEDPUBLIC-ICRPrinciple-FinalHyperlinks-revised Latest.pdf last accessed 26 February 2024.

- United Nations Commission on International Trade Law, UNCITRAL Model Law on Cross-Border Insolvency with Guide to Enactment and Interpretation, New York, United Nations (2014), p19.

- Idem, pp 27-32.

- United Nations Commission on International Trade Law, Status: UNCITRAL Model Law on Cross Border Insolvency (1997), https://uncitral.un.org/n/texts/insolvency/modellaw/crossborder_insolvency/status last accessed 26February 2024.

- United Nations Economic and Social Commission for Asia and the Pacific, Asia-Pacific Population and Development Report(2023), https://www.un.org/development/desa/pd/sites/ww.un.org.development.desa.pd/files/undesa_pd_2024_escap-reportpopulationdeveloment-17.pdf last accessed 20 April 2025.

- The authors would like to express their gratitude to Chan Wei Meng (Singapore), Giang Dinh (Vietnam), Hai Nguyen (Vietnam), Hajime Ueno (Japan), Handika Tjen (Indonesia), Jaufré Rouanet (UAE), Kotaro Fuji (Japan), Muhammed Ismail (Singapore), Pang Huey Lynn (Malaysia), Roderick John Sutton (Hong Kong), Trinh Hoang (Hong Kong), and Wong Chee Chien (Malaysia), and certain other insolvency practitioners (who chose to remain anonymous) for their contributions to the survey, which forms an integral part of this pape

- Steven T Kargman, Emerging Economies and Cross-Border Insolvency Regimes: Missing BRICs in the International Insolvency Architecture, Part I https://www.iiiglobal.

org/file.cfm/156/docs/navigating%20financial%20distress%20in%20emerging%20economies.pdf. - Ibid.

- Investment Monitor, Protectionism Likely to Continue Rising in 2025 (January 2025) https://www.investmentmonitor.ai/features/protectionism-likely-to-continue-risingin-

2025/#:~:text=Protectionism%20is%20expected%20to%20increase,trend%20to%20reshape%20global%20trade%3F. - Yeejin Jang, Jenny Jihyun Tak, and Wei Wang, “Global Insolvency and Cross-Border Capital Flows” (6 August 2024), UNSW Business School Research Paper https://

papers.ssrn.com/sol3/papers.cfm?abstract_id=4936763. - AN Yiannopoulos, Civil Law System: Louisiana and Comparative Law, 2nd ed, Claitor’s Publishing Reference (1999).

- Ibid.

- World Bank, Doing Business Report, https://archive.doingbusiness.org/en/data/exploretopics/resolving-insolvency.

- Jason Jack, “A Missing Variable: The Impact of Cross-Border Insolvency Laws on Foreign Direct Investment” (2018) Minnesota Journal of International Law 287 https:// scholarship.law.umn.edu/mjil/287.

- Report of the Committee to Strengthen Singapore as an International Centre for Debt Restructuring https://restructuring.bakermckenzie.com/wp-content/uploads/

sites/23/2016/11/Singapore-Report-of-the-Committee-4-20-16.pdf. - UNCITRAL-World Bank Group Judicial Capacity-Building Initiative on International Best Practices in Insolvency Law https://uncitral.un.org/sites/uncitral.un.org/files/

joint_programme_final_1.pdf. - Ibid.

- Yeejin Jang, Jenny Jihyun Tak, and Wei Wang, “Global Insolvency and Cross-Border Capital Flows” (6 August 2024), UNSW Business School Research Paper https://

papers.ssrn.com/sol3/papers.cfm?abstract_id=4936763. - Kazuhiko Yamamoto, “New Japanese Legislation on Cross-Border Insolvency as Compared with the UNCITRAL Model Law” (2002) 11 International Insolvency Review 67, 95.

- Sohsuke Takahashi, The Reality of the Japanese Legal System for Cross-Border Insolvency: Driven by Fear of Universalism (14 March 2011) https://www.iiiglobal.org/file. cfm/12/docs/2011_gold_prizepaper.pdf last accessed 26 February 2024.

- Guide to Enactment, para 104.

- RAFIP, article 21

- Guide to Enactment, para 150.

- Speech by Senior Minister of State for Law, Indranee Rajah, at the Regional Insolvency Conference (2014), https://www.mlaw.gov.sg/content/minlaw/en/news/ speeches/speech-by-sms-at-regional-insolvency-conf-2014.html last accessed 26 February 2024; Kannan Ramesh, Cross-Border Insolvencies: A New Paradigm, http:// www.supremecourt.gov.sg/Data/Editor/Documents/IAIR%202016%20Speech_Ramesh%20JC_delivered.pdf last accessed 26 February 2024.

- [2018] SGHC 16 (Singapore).

- [2024] SGHC(I) 1 (Singapore).

- 1997 Guide at para 89 and the 2013 Guide at para 104.

- (2019) 4 SLR 1343 (Singapore).

- Article 2(h) of the Third Schedule in Singapore’s Insolvency, Restructuring and Dissolution Act 2018.

- Re Ascentra Holdings, Inc, (2023) SGCA 32 (Singapore).

- See above, n 12.

- See above, n 3, p 95.

- Organisation for Economic Co-Operation and Development, Foreign Direct Investment for Development: Maximising Benefits, Minimising Costs (2002)

https://www.oecd.org/investment/investmentfordevelopment/1959815.pdf last accessed 26 February 2024. - See above, n 11.

- Sir Peter Millet, “Cross-Border Insolvency: The Judicial Approach” (1997) 6 International Insolvency Review 99, 109.

- Ibid.

- Beluga Chartering GmbH (in liquidation) vs Beluga Projects (Singapore) Pte Ltd, (2014) 2 SLR 815 [88] (Singapore).

- AC Network Holding Ltd v Polymath Ekar SPV1, [2023] ADGMCA 0002.

- Antonio M. Varvaro , Does the Application of the English Common Law Work in ADGM and DIFC? What is the Impact on Commercial Arbitration Cases? (11 October 2022) https://irglobal.com/article/does-the-application-of-the-english-common-law-work-in-adgm-and-difc-which-is-the-impact-on-commercial-arbitration-cases/.

- “Malaysia Plans to Implement the UNCITRAL Model Law on Cross Border Insolvency” (Legal advisory, tax consulting, audit services and management and IT consulting | Rödl & Partner) www.roedl.com/insights/newsflash-asean/2025_01/malaysia-implementation-uncitral-model-law-crossborder-insolvency accessed 8 May 2025.

- Mahalingam S, “Malaysia Forms Cross-Border Insolvency Reform Committee” (The Star, 6 February 2025) https://www.thestar.com.my/news/nation/2025/02/06/malaysia-forms-cross-border-insolvency-reform-committee accessed 8 May 2025.

- Oliver Massmann, “Legal Alert on the Draft of the Amended Law on Bankruptcy” (Insolvency/ Bankruptcy – Vietnam, 19 February2025)

https://www.mondaq.com/insolvencybankruptcy/1586958/legal-alert-on-

the-draft-of-theamended-lawonbankruptcy#:~:tex=According%20to%20the

20draft%2C%20secured,secured%20assets%20no%20longer%20exist.&text=Under%20the

%20Draft%2C%20Vietnamese%20courts,relevant%20to%20foreign%20bankruptcy%20proceedings. accessed 8 May 2025. - Ibid.

- Ministry of Corporate Affairs Office, Order No. 30/27/2018 – Insolvency Section, dated 23 January 2020.

- CBIRC, MCA, Report on the Rules and Regulations for Cross-Border Insolvency Resolution, June 2020, https://ibbi.gov.in/uploads/ resources/47fe7576712190d5554e2e50ce646e2f.pdf.

- Priyansh Verma, “IBC Amendment Bill Likely During in Monsoon Session, Cabinet Nod by End of April, Say Government Officials” (Moneycontrol, 11 April 2025). www.moneycontrol.com/news/business/ibc-amendment-bill-likely-during-in-monsoon-session-cabinet-nod-by-end-of-april-say-government-officials-12992137.html

accessed 8 May 2025.

* Mr. Saurav Panda is a Partner at Shardul Amarchand Mangaldas & Co. with specialisation in Insolvency & Bankruptcy, Debt Restructuring, Structured Finance, Corporate lending, Securitisations, debt issuances and strategic advisory on lender enforcement actions.

*Mr. Akham Khan is a Senior Associate at Shardul Amarchand Mangaldas & Co. in the Insolvency and Bankruptcy – National Practice Group.

Republished with permission from INSOL International. Originally published as Technical Paper No. 70, June 2025. © INSOL International 2025

Recent Posts

Judicial Reversals of Approved IBC Resolution Plans in India

Speech by the Guest of Honour at the 4th Annual Conference