ESG and Insolvency Risk: Evidence, Theory, and an Integrated Risk-Mitigation Framework

Prof. Himanshu Joshi*

Abstract

This study examines the role of Environmental, Social, and Governance (ESG) practices in mitigating corporate insolvency risk. Building on an extensive review of 69 empirical studies spanning 2005–2025, the paper synthesizes evidence on how ESG initiatives influence firm risk, including insolvency risk, earnings volatility, and broader financial and operational exposures. The literature indicates that strong ESG performance enhances operational efficiency, fosters stakeholder trust, reduces litigation risk, and facilitates access to external capital markets, collectively stabilizing cash flows and lowering insolvency risk. While leverage remains a key determinant of insolvency risk, ESG primarily operates through the cash flow channel, highlighting its distinctive contribution to corporate resilience. The study further identifies firm-level moderators—including CEO duality, board gender diversity, family ownership, stewardship practices, and financial constraints—that shape the effectiveness of ESG in reducing risk. The paper proposes an integrated framework that captures these interrelated channels and moderators, offering a comprehensive understanding of how ESG practices contribute to insolvency risk mitigation across diverse industries and geographies. By synthesizing theoretical perspectives, including stakeholder theory, resource-based view, signalling theory, and risk management theory, the study provides actionable insights for regulators, policymakers, investors, and corporate managers seeking to enhance firm stability and long-term value through ESG integration.

Keywords – ESG, Insolvency risk, Cash flow volatility, risk mitigation, corporate governance.

1. Introduction

On 29 January 2019, Pacific Gas & Electric Company and its publicly traded holding company, PG&E Corporation, filed for Chapter 11 bankruptcy in the United States Bankruptcy Court of Northern District of California. PG&E became the first major corporation to seek bankruptcy protection primarily due to liabilities arising from climate change–driven events. In 2015, Signal International, a U.S.-based marine services company, filed for Chapter 11 bankruptcy after facing multiple lawsuits alleging human trafficking and exploitation of migrant workers. One of the most infamous bankruptcies in global corporate history, Enron’s collapse (2001) was primarily the result of profound governance failures. Other cases of corporate failures on account of corporate governance issues include WorldCom (2002, USA), Satyam Computer Services (2009, India), and Wirecard (2020, Germany). Although these cases appear scattered across different regions and periods, they share a common thread—a failure to prioritize and integrate Environmental, Social, and Governance (ESG) practices into corporate strategy and operations.

ESG practices are commonly understood as firm-level policies and processes designed to manage risks and leverage opportunities related to environmental sustainability, social responsibility, and governance mechanisms. There is a growing recognition in the academic and practitioners’ literature that ESG factors directly affect a firm’s long-term financial performance1 and shareholders’ value.2 Under the ESG movement, investors are increasingly including ESG factors in their investment decisions alongside their conventional risk-return metrics.3 This trend facilitates easy access of capital to the firms with good ESG performance, leading to higher valuation,4 easier access to credit, and reputational benefits, among others. A growing body of literature also confirms that mainstreaming of ESG practice leads to reduction in several firm-level risks, such as systematic and operating risks,5 and default risk.6

Corporate insolvency, commonly defined as a firm’s inability to meet its contractual obligations to debt holders,7 can have severe consequences for shareholders, creditors, employees, customers, and regulators, among others. Insolvency risk arises when a firm’s future cash flows are insufficient to cover interest and principal repayment. Insolvency risk typically increases in two cases: first, when expected cash flows decline, or second, when they become more volatile. Given the critical implications of insolvency risk, it is important to explore whether ESG integration can serve as a mechanism to reduce such risk.

The existing literature on ESG and firm risk can be broadly categorized into two strands: (i) the impact of individual pillars—Environmental (E), Social (S), and Governance (G)—on firm creditworthiness, and (ii) the effect of the overall ESG score on mitigating insolvency risk. Within the first strand, researchers have found that the environmental component exerts the strongest influence in reducing risk, outperforming the social and governance dimensions.8 Strong governance has been shown to reduce total market risk,9 while environmental initiatives may shield firms from regulatory penalties and litigation.10 The second strand of research shows that higher ESG scores enhance a firm’s creditworthiness and thereby lower insolvency risk.11 Collectively, this body of evidence underscores that ESG practices—both at the pillar level and as a composite measure—play a meaningful role in reducing various dimensions of financial and operational risk.

The ESG–risk relationship has also been explored in country-specific contexts, including the United States, China, Japan, Korea, and emerging economies.12 Findings consistently indicate that higher ESG performance is linked to higher Z-scores, improved credit ratings, reduced default probability, and lower crash risk. Industry-specific studies report similar evidence in sectors such as tourism, family firms, oil and gas, and mining. Given the fragmented nature of the literature on ESG and firm risk—spanning diverse risk definitions and geographical contexts—this study aims to synthesize existing evidence and develop an integrative framework that elucidates the mechanisms through which ESG practices contribute to risk mitigation, with a particular emphasis on insolvency risk. Accordingly, the study pursues the following research objectives:

(i) To synthesize the extant literature on ESG and firm risk, with a particular focus on insolvency risk.

(ii) To propose an integrative framework that explicates the channels through which ESG practices reduce insolvency risk.

2. Methodology

We follow the three-step method, namely the thematic analysis, to identify, analyse, and review our selected papers.13 Unlike PRISMA, which serves as a reporting guideline for systematic reviews in medical sciences, the three-step analysis is a methodological approach used in qualitative research synthesis. Medical research focuses on well-defined research questions and follows a structured, replicable process, whereas social science research allows for more exploration and adaptation in the literature review process. In applying Tranfield’s method, we focused specifically on empirical studies examining ESG practices and their relationship to risk. Our analysis proceeded in three steps: planning the review, conducting the review, and synthesising the evidence.

Step 1 – Planning the review. The first step in planning the review was to identify and select the relevant databases. For this study, we used three major electronic databases: Web of Science, Scopus, and ScienceDirect. The main reason for choosing three databases is to collect the maximum sample possible to expand our research.

Step 2 – Conducting the review. The selection of keywords is based on the risks that any firm faces due to micro or macro factors. The finalised list of keywords includes “ESG” AND “RISK” OR “ESG” AND “OPERATI*” OR “ESG” AND “FIRM RISK” OR “ESG” AND “DEFAULT*” OR “ESG” AND “SYSTEMATIC” OR “ESG” AND “IDIOSYN*” OR “ESG” AND “BANKRUPTCY” OR “ESG” AND “INSOLVENCY”. In the initial search, we obtained 538 papers, from which we excluded book chapters, non-English publications, and other subject areas. We focused on management, finance, law, and environmental science subject areas. After duplication removal and abstract screening, our final sample consists of 69 studies from 2005 to 2025. Table 1 reports the number of studies screened.

Step 3 – Synthesizing the Evidence. Each study was examined in depth, and we recorded: (a) descriptive information, including year of data, context, type of firms, methods used, and event study mediators/moderators; and (b) theoretical underpinnings, outlining arguments both for support and against the relationship between ESG practices and risk.

Table 1: Number of Studies Screened

Stage

Total

Number of Studies

Total studies found in initial search

538

Web of Science

410

Scopus

128

Excluded (books, non-English, other subject areas)

−(134)

Remove duplicates

−(60)

Studies whose abstracts were read

344

Excluded after reading abstract

−(178)

Studies whose introduction and findings were read

166

Excluded (review papers)

12

Excluded (not related to risk)

85

Final sample included for review

69

3. ESG and Risk – Theoretical Underpinnings

A closer examination of the 69 studies reveals that 36 focus exclusively on ESG, 25 examine both ESG and its individual pillars, 6 investigate only the environmental pillar, 1 focuses on only the social pillar, and 1 explores the impact of the governance pillar on risk. A total of 23 theories are employed to discuss the relationship between ESG and risk.

Several theoretical perspectives explain how ESG practices are linked to risk. From the angle of stakeholder theory, companies can only thrive if they acknowledge their responsibility to consider the interests of all stakeholders, not just shareholders.14 By actively pursuing ESG initiatives, companies build moral capital—a kind of trust and goodwill—that can serve as protection in tough times. This connects closely with risk management and mitigation theory: strong ESG performance cushions companies during adverse market conditions,15 as it promotes stakeholder loyalty, helps avoid penalties and sanctions, and reduces the chances of unpredictable cash flows in the future.16

Legitimacy theory views ESG practices as a way for companies to demonstrate that their actions are proper and acceptable. By openly sharing information about their ESG efforts through voluntary disclosure, companies reduce the information gap between themselves and the public. This improves credit ratings and helps lower both idiosyncratic and systematic risks. Resource-based theory suggests that companies have internal dynamic capabilities that allow them to handle threats to their long-term survival. Resource-dependence theory argues that strong ESG performance helps companies satisfy the expectations of external funding providers—such as governments and banks—thereby reducing funding constraints.17

Agency theory offers contrasting explanations for the ESG–risk relationship. From a positive perspective, ESG practices can mitigate agency problems by reducing information asymmetry between principals and agents and by aligning the interests of various stakeholders.18 Conversely, managers may overinvest in ESG or CSR activities to serve personal interests rather than shareholder or stakeholder value, which can increase risk.19 Consistent with the positive tenets of agency theory, signalling theory suggests that firms convey their commitment to ethical and sustainable practices through ESG disclosures, thereby reducing perceived firm risk.20 Moderate ESG initiatives can lower firm risk by enhancing transparency, legitimacy, and stakeholder trust, whereas excessive or strategically misaligned ESG spending may increase costs, reduce financial performance, and elevate firm risk.

4. ESG and Insolvency Risk – A Proposed Framework

Table 2 summarizes findings from multiple studies examining the link between ESG and different measures of insolvency risk. These studies employed both market-based measures—such as credit default swaps, distance-to-default, credit ratings, and bond yield spreads—as well as accounting-based measures, including the Altman Z-score, Zmijewski ZM-score, Ohlson O-score, and earnings volatility.

Table 2: Association Between Measures of Insolvency Risk with ESG

Variable

Country

Type of Firm

Association with ESG

Default Risk

China

All firms

Negative

Distance to Default23

Global

Non-financial

Negative

Z-Score11

Europe

Non-financial

Negative

ZM Score25

USA

All firms

Negative

O-Score25

USA

All firms

Negative

Yield to Maturity22

Europe, N. America & Asia

All firms

Negative

Credit Ratings24

China

Non-financial

Positive

Litigation Risk26

China

Non-financial

Negative

Probability of Default26

Japan

Non-financial

Negative

Earnings Volatility8

China

Non-financial

Negative

Credit Default Spread3

USA

Non-financial

Negative

Bond Credit Spread21

China

Non-financial

Negative

Studies relying on market-based indicators—including credit default spreads,3 bond credit spreads,21 and yield to maturity22—generally find a negative relationship with ESG, implying that investors perceive firms with stronger ESG performance as less risky. The distance-to-default measure23 also shows a negative association, reinforcing the view that ESG contributes to greater financial stability and lowers default probability. By contrast, research using credit ratings24 reports a positive link with ESG, consistent with the argument that stronger ESG engagement enhances firms’ credit quality as recognized by rating agencies.

Analyses employing Altman’s Z-score,11 Zmijewski’s ZM-score, and Ohlson’s O-score25 consistently identify a negative association with ESG, indicating that firms demonstrating stronger ESG performance are correspondingly less prone to financial distress. Similarly, earnings volatility8 exhibits a downward trajectory in relation to higher ESG engagement, suggesting that robust ESG practices contribute to more predictable and stable financial outcomes. Both litigation risk26 and the probability of default27 are negatively associated with ESG, further implying that ESG practices serve not only to mitigate exposure to insolvency and default risk but also to reduce broader categories of financial and non-financial risk. Collectively, these findings reinforce the view that ESG constitutes a meaningful mechanism for enhancing corporate resilience and stability. Overall, evidence shows a negative association between ESG and insolvency risk, consistent across countries and industries.

Examining the role of green innovation—a key component of the environmental pillar—researchers found that eco-innovation significantly mitigates default risk, with the effect being more pronounced in market-based economies than in bank-oriented economies.11 Effective ESG reporting serves as a positive signal, consistent with signalling theory, that a firm is “doing good” by prioritizing the interests and well-being of its stakeholders. Moreover, ESG disclosures can increase the confidence of lenders, creditors, and equity investors, ultimately resulting in lower costs of debt, equity, and overall capital, thereby enhancing firms’ capacity to raise external debt.

4.1 Moderating Factors

Research reported that board gender diversity positively moderates the negative association between ESG performance and firm risk—strengthening the risk-mitigating effect of ESG for firms having a higher percentage of women on the board.10 Further, CEO duality—when the firm’s CEO also serves as board chair—can foster risk-increasing behavior, as powerful CEOs may prioritize personal financial benefits over ESG performance.28 In such cases, ESG disclosure plays a critical role in disciplining management and aligning the interests of shareholders and stakeholders. For Chinese firms, studies report that firm-level transparency and disclosures moderate the positive relationship between ESG performance and credit ratings, enhancing the creditworthiness benefits of ESG for more transparent firms.

A study investigated the impact of ESG performance on the insolvency risk of family firms.16 Analysing a global sample of the largest family firms, the study finds that higher ESG scores—especially in the environmental and social dimensions—are linked to lower insolvency risk. Ownership concentration exhibits an inverted-U relationship with insolvency risk, whereas a greater proportion of family members on the board is associated with lower firm stability. Financial constraints further moderate the ESG–insolvency risk link, with firms facing fewer constraints benefiting more from ESG initiatives.

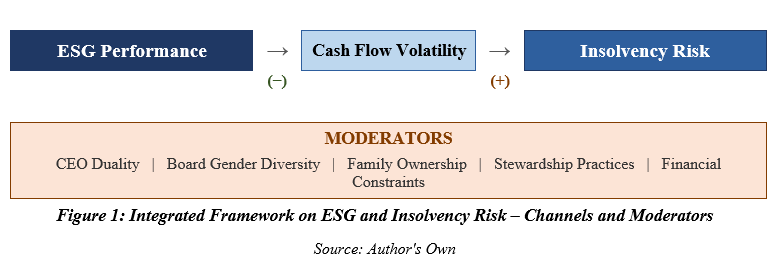

4.2 Integrated Framework

Building on the empirical evidence and theoretical insights discussed above, ESG performance can influence corporate risk through multiple interrelated channels. These include managerial incentives, governance structures, ownership concentration, board composition, and financial constraints, all of which shape how ESG initiatives are implemented and how effectively they mitigate insolvency risk. We therefore propose an integrated framework, presented in Figure 1 below, that illustrates how ESG performance can lower insolvency risk by operating through these organizational, governance, and financial channels.

The framework delineates the role of ESG in mitigating insolvency risk through the cash flow volatility channel, along with the moderating factors that shape this association. Insolvency risk primarily arises from two sources: cash flow volatility and excessive leverage. While leverage remains an important determinant, the framework emphasizes that ESG performance contributes to risk mitigation primarily by stabilizing cash flows, thereby reducing earnings uncertainty and enhancing financial resilience. This mechanism operates without directly altering the leverage channel, underscoring the distinctive contribution of ESG to insolvency risk reduction.

Strong ESG practices enhance operational efficiency and build stakeholder trust while simultaneously reducing litigation exposure. Collectively, these effects promote greater cash flow stability, which in turn mitigates insolvency risk. Empirical evidence further indicates that robust ESG performance improves access to external capital markets and lowers the cost of capital, thereby strengthening a firm’s debt-bearing capacity. This relationship is grounded in stakeholder theory, which emphasizes the value of stakeholder engagement; legitimacy theory, which underscores the role of corporate credibility and social acceptance; and risk mitigation theory, which explains how ESG practices reduce exposure to operational, legal, and reputational risks.

The extant literature suggests that several firm-level characteristics moderate the relationship between ESG practices and cash flow volatility. CEO duality—the separation of the roles of CEO and board chair—reduces managerial risk-taking and enhances ESG performance, particularly when CEO and board compensation is linked to the creation of environmental and social value.10 Board gender diversity, measured by the proportion of women on the board, strengthens the link between ESG performance and cash flow stability. Family-owned firms often prioritize the preservation of socio-emotional wealth (SEW), which reduces litigation risk, legitimizes corporate actions, and fosters stakeholder trust, collectively contributing to lower cash flow uncertainty.16

Firms with strong stewardship practices prioritize responsible management and accountability, strengthening stakeholder trust and enhancing the effectiveness of ESG initiatives in reducing cash flow uncertainty. Finally, firms experiencing financial constraints rely heavily on ESG practices to maintain operational stability and stakeholder trust, positively moderating the association between ESG performance and cash flow volatility.

5. Recommendations for Corporates and Regulators

Corporates should integrate ESG considerations into their core strategy and risk management processes, considering ESG not only as a corporate social responsibility but as a key mechanism for financial stability. Strengthening governance structures—such as separating the roles of CEO and chair of the board, linking executive compensation to environmental and social performance, and promoting gender diversity on the corporate board—can enhance the effectiveness of ESG initiatives in mitigating cash flow volatility and insolvency risk. Family-owned firms can leverage socio-emotional wealth priorities to align ESG adoption with long-term value creation. Additionally, transparent ESG reporting and disclosure are essential for reducing information asymmetry, improving investor confidence, and lowering the cost of capital, particularly for firms facing financial constraints.

Policymakers and regulators play complementary roles in creating a conducive environment for ESG integration. Regulators should ensure transparency, accountability, and consistency in ESG reporting by establishing standardized disclosure frameworks, which enhance comparability across firms and industries and support more informed investor decision-making. Bankruptcy and insolvency boards worldwide should consider incorporating ESG disclosures and performance indicators into their insolvency risk monitoring frameworks and early-warning systems. Such integration would facilitate the timely identification of firms at risk of financial distress due to weak governance, environmental lapses, or social non-compliance. Based on this early detection, pre-packaged insolvency resolution plans can be implemented, allowing distressed firms to maintain operational continuity and thereby minimizing value erosion.

Globally, several jurisdictions are increasingly recognizing the relevance of ESG considerations within insolvency and restructuring frameworks. In the European Union, the Corporate Sustainability Reporting Directive (CSRD) mandates that large companies disclose environmental, social, and governance information, thereby informing decisions in distressed situations. In the United Kingdom, the Corporate Insolvency and Governance Act 2020 emphasizes company viability and creditor interests, indirectly encouraging stakeholders to factor ESG performance into insolvency assessments. In India, the introduction of SEBI’s Business Responsibility and Sustainability Report (BRSR) for the 1,000 largest firms offers a valuable opportunity to incorporate ESG disclosures into the Corporate Insolvency Resolution Process (CIRP), thereby enhancing transparency and informed decision-making. Together, these developments highlight the growing convergence between ESG disclosure, credit risk assessment, and insolvency regulation. By integrating ESG performance into financial and legal oversight mechanisms, regulators can enhance early detection of financial distress, support sustainable corporate behavior, and strengthen the resilience of markets worldwide.

References

- Gunnar, B. Timo and B. Alexander, “ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies” (2015) 5(4) Journal of Sustainable Finance & Investment, 210.

. J. Nollet, G. Filis and E. Mitrokostas, “Corporate Social Responsibility and Financial Performance: A Non-Linear and Disaggregated Approach” (2016) 52 Economic Modelling 400–407.

- Atif and S. Ali, “Environmental, Social and Governance Disclosure and Default Risk” (2021) 30(8) Business Strategy and the Environment 3937–3959.

- De La Fuente, M. Ortiz and P. Velasco, “The Value of a Firm’s Engagement in ESG Practices: Are We Looking at the Right Side?” (2022) 55(4) Long Range Planning 102143.

- . E. Van Duuren, A. Plantinga and B. Scholtens, “ESG Integration and the Investment Management Process: Fundamental Investing Reinvented” (2016) 138(3) Journal of Business Ethics 525.

- H. Jamil and M. J. Khan, “Do Corporate Environmental Protection Efforts Reduce Firm-level Operating Risk? Evidence from a Developing Country” (2024) 33(3) Business Strategy and the Environment 4480–4492.

- Philip, “Strategic Default, Debt Structure, and Stock Returns” (2016) 51(1) Journal of Financial and Quantitative Analysis 197.

. J. Feng, J. W. Goodell and D. Shen, “ESG Rating and Stock Price Crash Risk: Evidence from China” (2022) 46 Finance Research Letters 102476.

- C. E. Bannier, Y. Bofinger and B. Rock, “Doing Safe by Doing Good: Non-Financial Reporting and the Risk Effects of Corporate Social Responsibility” (2023) 32(4) European Accounting Review 903.

- H. Shakil, “Environmental, Social and Governance Performance and Financial Risk: Moderating Role of ESG Controversies and Board Gender Diversity” (2021) 72 Resources Policy 102144.

- Meles, D. Salerno, G. Sampagnaro, V. Verdoliva and J. Zhang, “The Influence of Green Innovation on Default Risk: Evidence from Europe” (2023) 84 International Review of Economics & Finance 692–710.

- Caiazza, G. Galloppo and G. La Rosa, “The Mitigation Role of Corporate Sustainability: Evidence from the CDS Spread” (2023) 52 Finance Research Letters 103561.

- Tranfield, D. Denyer and P. Smart, “Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review” (2003) 14(3) British Journal of Management 207.

- E. P. Y. Yu and others, “Environmental Transparency and Investors’ Risk Perception: Cross-Country Evidence on Multinational Corporations’ Sustainability Practices and Cost of Equity” (2021) 30(8) Business Strategy and the Environment 3975.

- . M. K. Hassan, L. Chiaramonte, A. Dreassi, A. Paltrinieri and S. Piserà, “Equity Costs and Risks in Emerging Markets: Are ESG and Sharia Principles Complementary?” (2023) 77 Pacific-Basin Finance Journal 101904.

- P. Maquieira, J. T. Arias and C. Espinosa-Méndez, “The Impact of ESG on the Default Risk of Family Firms: International Evidence” (2024) 67 Research in International Business and Finance 102136.

- C. Fu, C. Yu, M. Gu and L. Zhang, “ESG Rating and Financial Risk of Mining Industry Companies” (2024) 88 Resources Policy 104308.

- Benlemlih, “Corporate Social Responsibility and Dividend Policy” (2019) 47 Research in International Business and Finance 114.

- Kuzey, A. Uyar and A. S. Karaman, “Over-Investment and ESG Inequality” (2023) 22(3) Review of Accounting and Finance 399.

- Z. X. Huang, “An Integrated Theory of the Firm Approach to Environmental, Social and Governance Performance” (2022) 52(S1) Accounting & Finance 1567.

- Lian, T. Ye, Y. Zhang and L. Zhang, “How Does Corporate ESG Performance Affect Bond Credit Spreads: Empirical Evidence from China” (2023) 85 International Review of Economics & Finance 352–371.

- Baldi and A. Pandimiglio, “The Role of ESG Scoring and Greenwashing Risk in Explaining the Yields of Green Bonds: A Conceptual Framework and an Econometric Analysis” (2022) 52 Global Finance Journal 100711.

- A. Anand, R. Vanpée and I. Lončarski, “Sustainability and Sovereign Credit Risk” (2023) 86 International Review of Financial Analysis 102494

- Wang and L. Yang, “Environmental, Social and Governance Performance and Credit Risk: Moderating Effect of Corporate Life Cycle” (2023) 80 Pacific-Basin Finance Journal 102105.

- Boubaker, A. Cellier, R. Manita and A. Saeed, “Does Corporate Social Responsibility Reduce Financial Distress Risk?” (2020) 91 Economic Modelling 835–851.

- Kuang and C. Luo, “Corporate ESG Performance and Litigation Risk – Based on ESG Lawsuits of Listed Firms in China” (2025) 32(9) Applied Economics Letters 1300–1305.

M. Kanno, “Does ESG Performance Improve Firm Creditworthiness?” (2023) 55 Finance Research Letters 103894.

. E. Palmieri, G. B. Ferilli, V. Stefanelli, E. F. Gerett and M. Polato, “Assessing the Influence of ESG Score, Industry, and Stock Index on Firm Default Risk: A Sustainable Bank Lending Perspective” (2023) 57 Finance Research Letters 104274.

* Professor, FORE School of Management, New Delhi (himanshu@fsm.ac.in).

The author gratefully acknowledges the infrastructure support provided by FORE School of Management, New Delhi.

The author was invited to present the paper at the 3rd ILA Annual Conference held at the Tijara Fort Palace, Rajasthan, India, from 14–16 March 2026.

This is the abridged version of the paper published in the Journal of Business Law [Joshi, Himanshu. (2026). ESG and Insolvency Risk: Evidence, Theory, and an Integrated Risk Mitigation Framework. 2026. 107-125] under the guidance and support of Mr. Sumant Batra, Insolvency Lawyer; President, Insolvency Law Academy and Dr. Eugenio Vaccari, Chair, ILA ISF, Senior Lecturer in Law, Department of Law and Criminology, Royal Holloway, University of London, UK

Recent Posts

ESG and Insolvency Risk: Evidence, Theory, and an Integrated Risk-Mitigation Framework